5 Common Bookkeeping Mistakes Contract Workers Make (and How to Avoid Them)

Bookkeeping might not be the most glamorous part of being a contract worker, but it’s one of the most important. Your financial health depends on keeping things organized, accurate, and compliant with tax requirements. Unfortunately, many freelancers and contract workers make avoidable mistakes that can lead to stress, penalties, or missed opportunities to save money. In this blog, we’ll tackle five common bookkeeping mistakes contract workers often make—and, more importantly, how you can avoid them to keep your finances running smoothly.

Nathan Stadler

1/21/20253 min read

5 Common Bookkeeping Mistakes Contract Workers Make (and How to Avoid Them)

Managing your books as a contract worker can feel like navigating a maze—daunting, confusing, and full of potential missteps. But don’t worry! By steering clear of these five common bookkeeping mistakes, you’ll not only simplify your financial life but also set yourself up for long-term success. Let’s dive in!

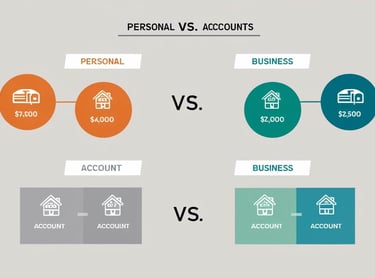

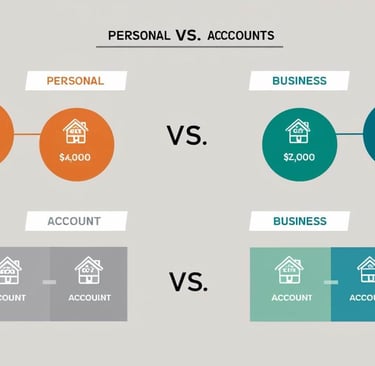

1. Mixing Personal and Business Finances

Running a business is already a balancing act, and adding financial management into the mix can feel overwhelming. You might think, "Why not just throw everything—personal and business finances—into one basket? It seems easier, right?" Wrong. When you mix your finances, you lose clarity, control, and valuable tax benefits. Trust me, it’s a fast track to chaos.

Your business deserves its own financial home—a dedicated bank account. Personally, I recommend Relay. It’s fee-free, integrates seamlessly with major software, and keeps things clean. When you need to pay yourself, transfer funds or set yourself up as an official employee and pay yourself a salary. This isn’t just about taxes; it’s about running your business like a pro. Plus, let’s be real—having a polished system feels amazing!

2. Forgetting to Track All Income

We’ve all been there: juggling projects, scrambling to meet deadlines, and forgetting to log smaller payments. But those overlooked dollars can cause major headaches later. Whether it’s a quick gig, a partial payment, or a side hustle, every cent matters. Skipping this step not only messes up your financial records but could also lead to tax issues or, worse, penalties.

Here’s the fix: Use bookkeeping software or an app to log every payment as soon as you receive it. Think of it like building a puzzle; even the smallest pieces matter to see the full picture of your financial health.

Pro tip: If you’re using QuickBooks, the Undeposited Funds account is your new best friend. It acts as a holding zone for money not yet deposited into your bank. It’s perfect for keeping tabs on what’s cleared versus what’s pending—a simple bridge to keep everything organized.

3. Neglecting to Save for Taxes

This one’s tough, I know. You work hard, you make money, and naturally, you want to keep as much as possible. But here’s the reality: some of that money isn’t yours—it’s the government’s. Ignoring this truth can leave you scrambling when tax season rolls around.

The solution? Make a habit of setting aside at least 10% of your earnings each month. By the time taxes are due, you’ll have a cushion ready to go. And hey, depending on the tax laws that year, you might even have a little left over! It’s all about staying ahead so taxes don’t hit you like a ton of bricks when you least expect it.

4. Failing to Keep Expense Receipts

Think of every receipt you collect as evidence—proof that your business deserves those sweet, sweet tax deductions. Without them, you’re walking a risky line. If the government suspects something’s off, an audit could be on the horizon. And trust me, no one wants to face that without proper documentation.

The good news? Staying organized isn’t as hard as it seems. Use apps or cloud storage to digitize your receipts. Create a simple system where you can easily access and categorize them. A little effort now will save you from a world of stress (and expenses) later.

5. Skipping Regular Bookkeeping Check-Ins

Let’s be honest—your books can feel like the monster under the bed. Sometimes it’s easier to avoid them than face the truth about where your money’s going. But here’s the thing: your books aren’t out to scare you; they’re there to guide you.

Take time each week or month to review your finances. It’s not just about catching mistakes—it’s about understanding your cash flow so you can make it work for you. When you know how your money is moving, you have the power to steer it in the right direction. Trust me, the insights you gain are worth every minute you spend.

Final Thoughts

Bookkeeping doesn’t have to be overwhelming. By avoiding these common mistakes, you’ll bring order to your finances, stay on top of taxes, and set yourself up for success.

I’d love to hear your thoughts! Drop a comment if this resonated with you or if you have any advice to share. Collaboration is my favorite part of this journey—let’s learn and grow together!

Connect

Support

Books Balancer Bookkeeping

Yakima, WA

nate@booksbalancer.com

509-581-6435

© 2024. All rights reserved.